I have been on both sides of this for a while now. I make vermouth in South London with a team of six. I also build the AI tooling that sits behind a handful of small drinks businesses, the kind of producers who cannot run a pricing team because the same person who tastes the batch also signs off the price.

So when The Spirits Business reported in May that Spiros Malandrakis at Euromonitor called the end of indefinite premiumisation, I read it twice. Not because it was a surprise from the bench. We have been feeling it. But because it is the first time a major research house has said it out loud.

From the production floor, here is what changes when "premium value" replaces "premium price" as the working frame.

What premium value actually means in a small operation

Nedstar's Q4 2025 analysis uses the term explicitly. Consumers still want quality and story, but they will not pay indiscriminately. Euromonitor's own March 2024 forecast had already flagged this. The upper end of spirits is becoming a tougher environment as household finances stay under pressure.

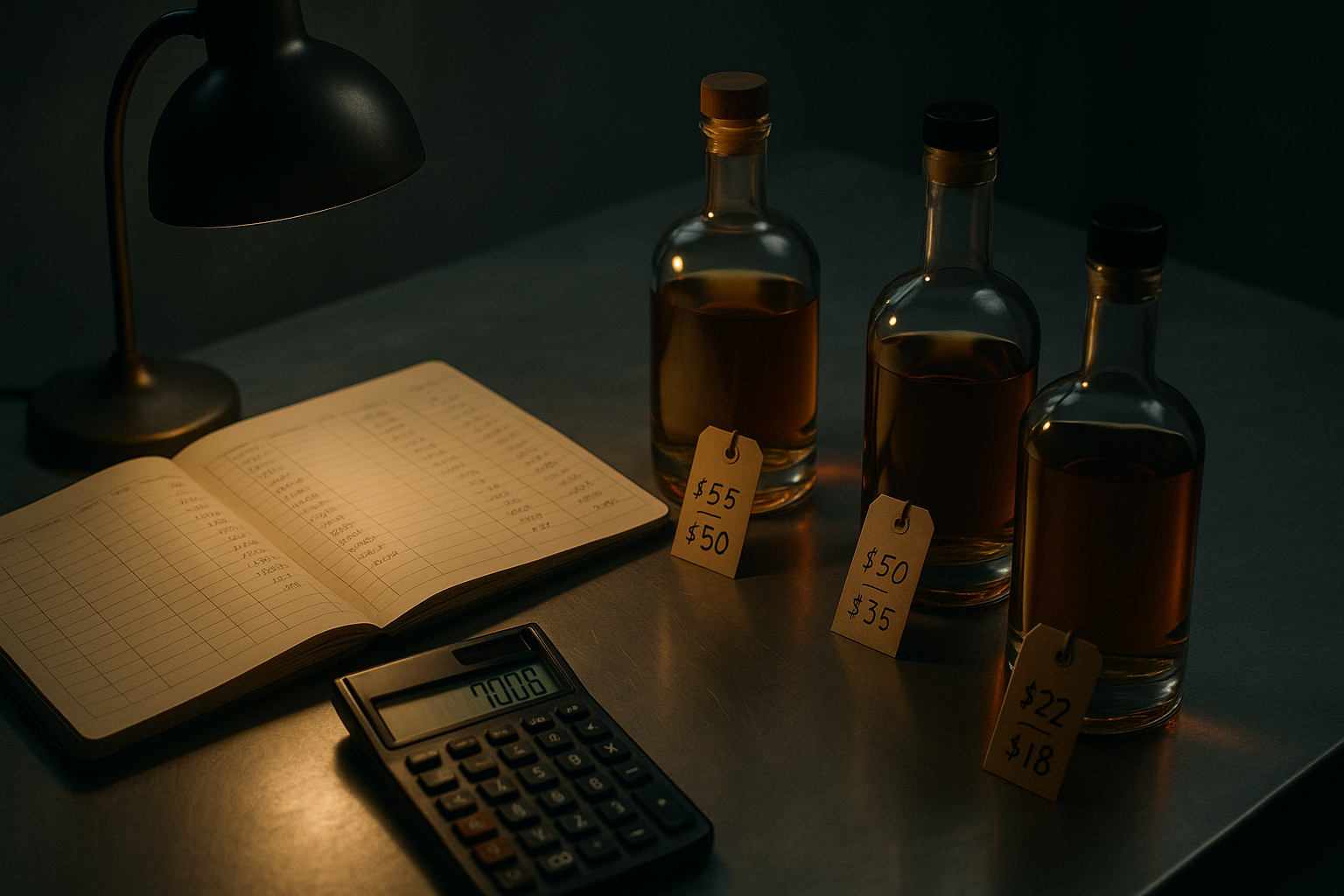

Translation for a small producer: the £35 bottle that used to sell on craft credentials alone now has to prove its arithmetic. What does the £35 buy that the £22 doesn't? If you can answer that with specific production decisions, botanical sources, batch sizes, ageing time, the bartender feedback that shaped the recipe, you are selling premium value. If you cannot, you are hoping the label does the work for you.

I want to be honest about something here. For most of the last decade, small craft producers have not had to do that arithmetic explicitly. The premiumisation trend covered for fuzzy thinking. You could price a new SKU based on what felt right alongside competitors and trust the rising tide. That period is closing.

The pricing-intelligence gap that small brands hit

Here is the pattern we see across the brands we build tooling for. They have product-level pricing intuition. The owner can tell you within 10p where a new bottle should sit. What they do not have is the layer that connects that intuition to weekly data. Which SKU's margin compressed last month. Which trade account stopped reordering at the old price. Which retail channel is absorbing duty rises and which is passing them straight through.

That gap is partly about tooling. The volume just is not there to justify a £20k-a-year pricing platform built for the spirit majors. Diageo and Pernod Ricard run revenue-growth-management teams whose annual budget exceeds most small distilleries' total turnover. Their pricing infrastructure is not proportionate.

But the gap is also about cadence. Most small drinks businesses see margin data quarterly, when the accounts close, by which point the corrective action is already late. The decisions that needed pricing intelligence happened in week 3, when a new account placed its first order, or week 7, when a retailer asked for a margin top-up.

The duty squeeze compounds everything

The timing makes this sharper. The Morning Advertiser tracked the rise: duty on spirits is up over 18% since the new alcohol duty system was introduced in August 2023. The February 2026 RPI-linked increase added another 3.66%. The House of Commons Library briefing on alcohol duty confirms the trajectory.

When your cost base rises structurally, you cannot price your way out. Your venues face the same squeeze. They need products that move at price points customers accept, not products that sit on back bars while cheaper alternatives turn faster. The margin conversation between you and your trade account is happening every month now, not every year.

What we track instead of vanity metrics

The brands we build tooling for do not track follower counts. They track three things on a rolling weekly basis: velocity per stockist (how fast each retail or trade account is moving stock), repeat-order interval (how long between reorders for each account, and how that is drifting), and effective margin after promo (the actual margin after every discount, sample drop, and trade rebate is netted out).

None of those are sophisticated metrics on their own. The work is in the connecting tissue: pulling Shopify, the venue invoicing system, and the trade promo log into one weekly snapshot so the owner can see all three together. That is the layer we build. It is not glamorous. It is the layer most small drinks businesses do not have time to build for themselves, and that legacy ERP vendors do not bother building because the volume is not there.

| Positioning | What it relies on | Risk level in 2026 |

|---|---|---|

| Luxury premiumisation | Brand mystique, scarcity, high margins | High. Consumers trading down, duty rising. |

| Premium value (mid-premium with demonstrated utility) | Production transparency, craft credentials, operational data | Moderate. Requires investment in intelligence layer. |

| Commodity positioning | Volume, price competition | High. Race to the bottom, low loyalty. |

The middle row is the one most small producers think they are already in. The honest test is whether they have the operational data to defend the position when a buyer asks. If the answer is "we just feel it should be £35", they are closer to luxury premiumisation than they realise, and exposed to the trade-down pressure Malandrakis describes.

Where Absolution Labs comes in

This is where Absolution Labs comes in. We bring the pricing-intelligence layer to small drinks businesses that already have the product instinct but do not have the technical infrastructure to back it weekly. The tooling watches velocity, margin, and reorder cadence per account, surfaces the drift before it hits the quarterly P&L, and gives the owner enough specifics to defend the price in the next trade conversation.

What it does not do is set the price. The price is still a craft decision, anchored in what the bottle actually costs to make, what the story carries, and what the room will bear. The tooling makes the decision defensible with data, which is what "demonstrated value" looks like in practice.

The other thing worth saying. Honestly, fair enough. Most small drinks businesses we talk to are tired of being sold software. They have watched the platform-and-dashboard cycle for ten years. What they actually want is the operational answer to a specific question: "is this account still profitable at the post-duty number?" The tooling stays small and answers the specific questions. We are not building another general-purpose CRM.

Frequently asked questions

What does "premium value" actually mean for spirits pricing?

Premium value is Nedstar's term for the shift from open-ended premiumisation to customers expecting genuine quality plus story plus demonstrated utility in exchange for a higher price. The producer has to prove the £35 is not just the £22 with a better label.

Has UK alcohol duty really risen 18% since 2023?

Yes. The Morning Advertiser tracked the rise: spirits duty is up over 18% since the new alcohol duty system was introduced in August 2023. The February 2026 RPI-linked increase added another 3.66%. The House of Commons Library publishes the full trajectory in its alcohol duty briefing.

What pricing data should a small drinks business track weekly?

Three things at minimum: velocity per stockist, repeat-order interval, and effective margin after promo (the actual margin after every discount, sample drop, and trade rebate is netted out). Watching those three rolling means margin compression surfaces before the quarterly P&L instead of after.

Can AI replace a pricing team for a small drinks brand?

No, and that is the wrong frame. AI tooling at this scale is not a substitute for the owner's product instinct. It is a substitute for the £20k-a-year revenue-growth-management platform that is built for spirit majors and overkill for a six-person operation. The tooling surfaces the data; the owner still sets the price.